Recession, recovery and reform

Speech

Chair Michael Brennan delivered a speech to the Property Council in Canberra on 26 May 2021.

Download the speech

Read the speech

I want to talk to you today about the 3Rs: recession, recovery and reform.

The pandemic and the recession remind us that pessimism sells. This time last year it was regarded as slightly naïve to express faith in a V-shaped recovery.

A lot of pundits offered up a lot of other letters of the alphabet: U-shaped, W-shaped, L-shaped, even I-shaped.

Our official macro-economic family in the Treasury and Reserve Bank were closer to the truth – and they were helped by real time data from a range of sources, not least of which was the single touch payroll data collected by the ATO and used by the ABS to illustrate labour market impacts in close to real time.

This tech-enabled innovation was not available to policy makers in the early 1990s or even to the same extent during the GFC.

This might sound off-message for a microeconomist, but it really matters how well an economy handles and then rebounds from a recession.

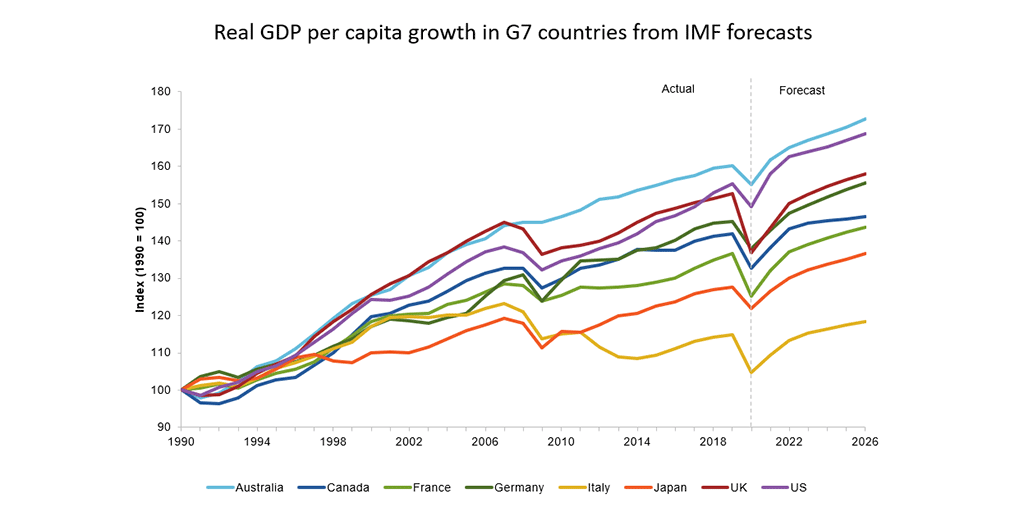

This first slide tracks GDP per capita for Australia and the G7 economies.

What it tells you is that Australia has outpaced all of the G7 in real per capita growth since 1990 because:

- this is per capita, it strips out the impact of population growth

- it is real GDP growth; it strips out the impact of movements in Australia’s terms of trade.

It illustrates that the gap between Australia and our large, developed economy peers has multiple drivers:

- Faster productivity growth in the 1990s, which set us on a steeper upwards trajectory.

- Avoiding recession during the GFC, when others dipped and never fully recovered.

- According to IMF forecasts, (so far) a milder recession and stronger rebound from the current recession.

By contrast, you can see that the European economies never fully recovered from the double dip recession of the GFC and Euro crisis.

The US lost a lot of ground in the GFC but are making much of this up, with a strong anticipated rebound from COVID. Noting that the US is still the richest country in this dataset in absolute terms.

The UK economy grew rapidly in the 1990s but has lost considerable ground during the pandemic.

France and Germany are projected to recover more slowly from the pandemic. On IMF projections, Italy will have a lower GDP per capita in 2026 than it had in 2006. A remarkable result.

So twice in the last 12 years, Australia has weathered a global economic crisis better than almost all of its developed economy peers.

And we have ‘banked’ some of that gain in the form of higher cumulative real GDP growth. We went into the last two global crises with strong fiscal buffers, well capitalised banks, comparatively flexible labour markets and an openness to trade, all of which helped support the response and recovery.

It seems fashionable in the moment to herald new economic paradigms, but in reality, the broad economic framework which Australia has developed and had in place for the last 30 years, has been vindicated by events.

It laid the groundwork for the macro-economic response to the crisis itself, which of course had to be tailored to precise circumstances.

Every crisis, and every recession is different.

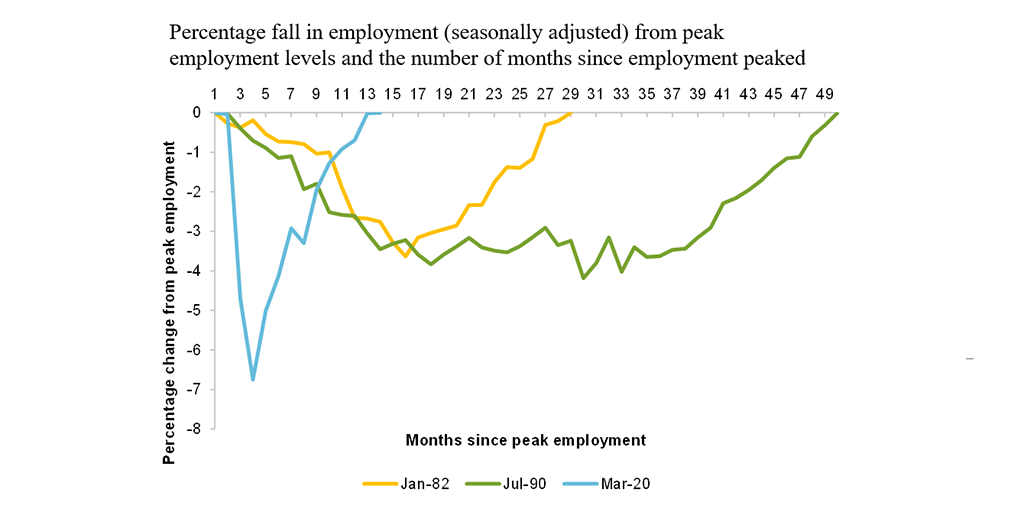

This chart shows the path of employment in the last 3 recessions in Australia: the early 80s, the early 90s and today.

It shows how many months it took for employment to return to its pre-recession levels: 29 months in the early 1980s; more than 4 years in the early 1990s and 12 months this time – despite a much bigger reduction peak to trough.

The rebound in employment reflects the remarkable recovery in the labour force participation rate (back to pre-pandemic levels) and a fall in unemployment to just above pre-pandemic levels.

The other shock-absorber in the labour market – as with the GFC – was hours worked per employee which fell by more than the fall in employment and had almost recovered to pre-pandemic levels by December 2020.

This was in stark contrast to the experience of the early 1990s where most of the labour market weakness manifested in job losses. In 2020, more of the load was borne by a reduction in hours worked, due to a combination of labour market flexibility and JobKeeper.

The implications of the pandemic and the recession for productivity remain to be seen.

Over the long run, productivity growth is the key to rising living standards. In the short term, particularly in the midst of a recession, with unemployment and idle resources, productivity is not necessarily a good guide to wellbeing.

What matters is productivity growth over the next 5 to 10 years as we emerge from this episode.

In 2019-20, oddly enough, labour productivity actually rose by 0.5 per cent. This is partly a quirk, reflecting that in many industries output fell by less than employment did – hence output per hour worked actually rose.

It also reflects the differential impact of the recession. It hit hardest in labour intensive service industries which have relatively low levels of productivity, while employment rose in some high productivity industries, like mining.

This will partly unwind as employment returns to the hardest hit service industries. In fact, on the face of it, there is less labour reallocation between industries, the longer the recovery progresses.

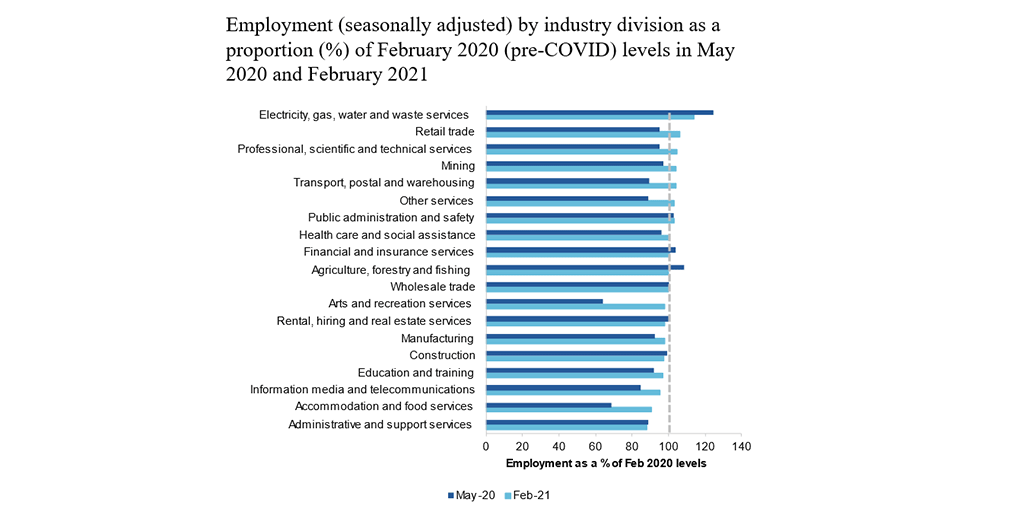

In May 2020, (the dark blue bars) the composition of employment across the economy had shifted a lot, with several industries well below their pre-COVID levels.

By February 2021, (the light blue bars) this effect had moderated, with most industries converging back towards their pre-pandemic employment levels.

At the level of smaller sub-industries, or individual firms, the story would be a bit different.

This reflects the impact of Jobkeeper and other fiscal supports like the cash flow boost, along with policies like interest deferral, rent deferral and relief and temporary changes to insolvent trading rules.

Insolvencies in 2020 were down on 2019 levels by around one third.

I have said in the past that the recession and recovery would entail some reallocation of labour and other resources across the economy. That remains true, though the process could be yet to fully play out, as temporary supports are withdrawn.

The overall focus of policy in 2020 was to hold things together, reflecting the nature of this recession.

Every recession is painful, but some have the consolation of a cleansing effect – where low productivity firms exit, and high productivity firms stay in business. Which can set the economy up for faster productivity growth in the recovery, as occurred in the 1990s (for a range of reasons).

The 2020 recession was of a different character. Unlike a conventional demand-side recession, it risked wiping out firms indiscriminately in the absence of government support.

It arguably meant that those fiscal measures couldn’t just take the form of demand-side stimulus but had to directly support the short term viability of firms and maintain the employment relationship.

Hence, we will no doubt see some reallocation of resources across the economy. Whether we see a productivity rebound due to significant exit of low productivity firms is less clear.

The good news about Australia’s performance relative to other economies comes with a qualification – namely our poor recent productivity growth by historical standards. Real growth in per capita GDP and incomes over the last decade has been the slowest in 60 years. In terms of income growth, the last decade has resembled the 1970s.

Of course in some ways, that is misleading – we are materially richer than we were in the 1970s and the Australian economy is more efficient and closer to the global frontier than it was then – prior to the reforms of the last 40 years. But it does serve as a caution against the view that our aim should be simply to rebuild the economy of 2019.

As I noted earlier, our broad policy framework is strong and should be maintained, not least because it facilitates economic adaptation and change. But it should not be the aim of public policy to restore every pre-existing business model that was disrupted by the pandemic. Not all of them were sustainable or desirable.

The true goal of economic policy is to create a more dynamic economy that can drive higher productivity and income growth into the future. It can do this by promoting a more efficient allocation of resources across the economy.

Much of the Productivity Commission’s recent work deals with driving greater competition and efficiency in key markets like superannuation, financial services, communications, agriculture and airports.

Inefficiencies in individual sectors can add up to an economy wide brake on living standards. But policy also plays a role in enabling innovation and the adoption of new technology.

Over the long term, productivity growth is largely driven by technological progress. That technological progress is about more than inventing new things; and more even than replacing old machines or inputs with a more up to date version.

Much of the value of technical progress comes in the changes to production techniques and business models which new inventions make possible – effectively the flow on effects, which themselves trigger new innovations.

The example of electricity is instructive. Thomas Edison invented the lightbulb in 1870 and had set up electricity generation plants in the early 1880s. But 20 years later, the vast majority of American factories still used steam power.

The take up of electric power took several decades. And the productivity gain did not come from the simple replacement of steam engines with an electric motor.

Instead, the productivity gain came from the reconfiguration of factories to take full advantage of what electrical power made possible – the ability to have lots of small machines with their own source of power, available when and where it was required.

The rise of electricity then spawned other inventions – new machines and household appliances for example – that only became possible because of this more flexible form of energy.

And the same can be said of digital technologies of today, including data analytics and AI.

As economists Erik Brynjolfsen, Daniel Rock and Chad Syverson noted that electricity, like AI, can be regarded as ‘general purpose technologies’. They make the point:

General purpose technologies (GPTs) are ‘engines for growth’. Specifically, they are pervasive, improve over time, and lead to complementary innovation (Bresnahan and Trajtenberg 1995).

However, along with installing more easily measured items like new types of physical equipment and structures, we emphasize that realizing their potential also requires large intangible investments and a fundamental rethinking of the organization of production itself.

Firms must create new business processes, develop managerial experience, train workers, patch software, and build other intangibles.

Hence the role of policy is to remove the potential barriers that stand in the way of that broader technological adoption – the new business processes and complementary innovations. Those barriers include the regulations or funding models or licensing schemes that entrench existing approaches.

There is much debate in the economics profession about whether the pace of technological progress is slowing down. Maybe the world is running out of ideas, or – more plausibly – new breakthroughs are getting harder and more costly to generate.

But the speed with which messenger RNA vaccines have been developed over the past year, or the dramatic falls in the price of renewable energy remind us that human inventiveness is a constant.

The question is whether we, as a society through our policy settings, embrace technological progress and its potential to transform existing business models and production processes.

Two forced innovations from the pandemic provide examples – telehealth and online education.

In its simplest form, telehealth is the replacement of a one-on-one physical consultation with a one-on-one remote consultation. It saves on transport and the time wasted in the so-called ‘waiting room’ (we estimate this downtime as costing around $1 billion a year). Similarly, for many school students in 2020, online education was essentially a classroom lesson that was filmed.

But in essence, this is the equivalent of replacing a single steam engine with a single electric motor. The real innovation comes as we explore all the ways digital communications can fundamentally change the nature of the service.

In health that would mean data linkages between GPs and hospitals, AI to pro-actively identify patients at risk of chronic disease, real time communications and information sharing between patients and clinicians. And these are just the foreseeable innovations.

One of the potential barriers to digital adoption is the funding model for primary care, which pays doctors primarily for one-on-one consultations, effectively locking in the existing mode of service delivery.

Recently the Productivity Commission released research on innovations in care for chronic health conditions. It examined real life case studies of enterprising people who are swimming against the tide of existing incentives and entrenched cultural practices in order to deliver more proactive, integrated and patient-centred care to those with chronic conditions.

In our mental health report, we discussed the important gap for low intensity services that can be filled by moderated online services, which economise on clinicians as part of a broader digital offering.

Two other forced experiments from the pandemic are the increase in working from home and the continued uptake of online shopping.

Both reflect the adoption of digital technology and both have the potential to be transformative and disruptive of existing business models to some extent.

Like electricity in the early 1900s, working from home relies on a technology that has been available for some time, but it took the pandemic to force an awareness of how it can be applied.

For 20 years prior to the pandemic, the share of the workforce working from home was remarkable steady at around 5 per cent. Last year during the pandemic it shot up to around 40 per cent. In the near term, the level of working from home will almost certainly be somewhere in between.

Working from home is not practical for many people – we estimate based purely on occupational requirements that around 40 per cent of jobs can in principle be done remotely. But whether it is economic to do those roles remotely depends on the individual worker and the individual firm.

There are trade-offs between the time savings of the commute (plus the flexibility of being able to combine work with other tasks) on the one hand and the loss of social connection and creativity that comes from physical co-location on the other. But the forced learning from the COVID pandemic has taught many that working from home can work, at least part of the time.

To invoke the electricity metaphor once again, the real productivity gain will come not from replicating at home the precise tasks previously performed in the office, but by changing both.

The true ongoing innovation may be less about where we work and more about how we work. The office will adapt – probably to be more focused on collaboration and team-based work. CBDs will innovate, to remain attractive locations for work and leisure.

It would be foolhardy to proclaim the death of the city. It is even possible that increased working from home could increase the concentration of office jobs in CBDs.

But it is equally futile to try and frustrate the natural tendency towards some increase in remote working. It is a natural, technologically enabled innovation that can work to the mutual benefit of firms and workers if worked through cooperatively.

The role of regulation – in areas like workplace health and safety and workplace relations – is to facilitate that cooperation rather than trying to lock in a legacy approach.

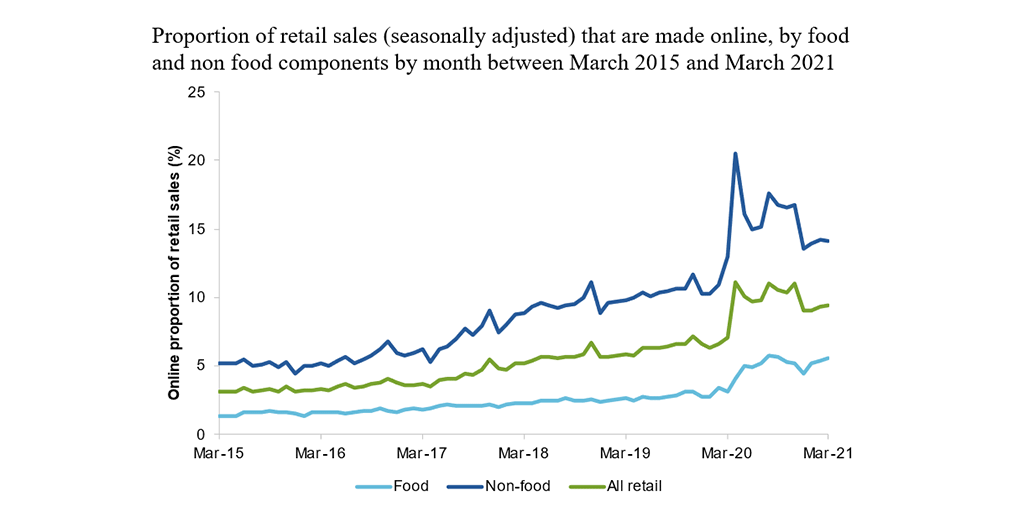

The story of online retail is similar.

As the chart shows, the online share of retail spending spiked during 2020 and has moderated since but is unlikely to return fully to its pre-pandemic levels. The online share of non-food retailing has doubled in less than 4 years. As to whether that trend is maintained, we can only speculate.

What we can say is that the increased uptake of digital technology during 2020 has created some uncertainty about the location of economic activity into the future.

The office will evolve, as will different forms of retail. The shift of industrial land from manufacturing to logistics may continue. Perhaps office and residential uses will blur.

But in the face of all that, we still have state planning systems that are highly prescriptive as to what different forms of economic activity can occur where

In particular, we observe a proliferation of commercial zone types and often a lack of uniformity about zone definitions across local government areas. The allowable uses in those zone types can be quite limited, with few ‘as of right’ uses (or even none).

Planning is a complex area. Passions can run high and opinions can differ – even within the Property Council. But some measured steps could help boost the flexibility of our economy in adapting to change.

In particular, we have proposed a number of areas for reform, including:

- ensuring that local plans (such as planning schemes or LEPs) can deliver on state-wide development and population objectives

- having fewer zone types with a broader range of allowable and as of right uses

- standardising permissible land uses within zone types across all LGAs

- having more defined and efficient processes for rezoning applications

- expanding the use of streamlined assessment tracks, by re-thinking what constitutes a low-risk application

- cutting DA assessment times through more concurrent decision making, streamlining the use of state referral agencies and using electronic lodgement and tracking of applications.

Even incremental progress on these fronts would position us to better respond to change and uncertainty. And would be consistent with the broad policy framework I mentioned earlier.

The broader question for regulatory policy is whether it stifles new innovation or embraces it, or – as in the case of Uber and ride sharing – starts with one and eventually, reluctantly, shifts to the other.

All this suggests that the path to higher productivity growth should not be seen as the quest for a policy El Dorado – a single big thing, or a destination flowing with riches. Rather, it is a whole lot of little things that potentially add up.

The challenge is that, because the path of innovation is unknown, we can’t identify ahead of time the precise regulatory barriers that will frustrate future growth. Nor can we quantify the benefit of their removal. It requires some faith in human ingenuity and the great unknown that is progress.

I reflected earlier that pessimism sells; but in the long run it is perhaps optimism that pays the bigger dividend.